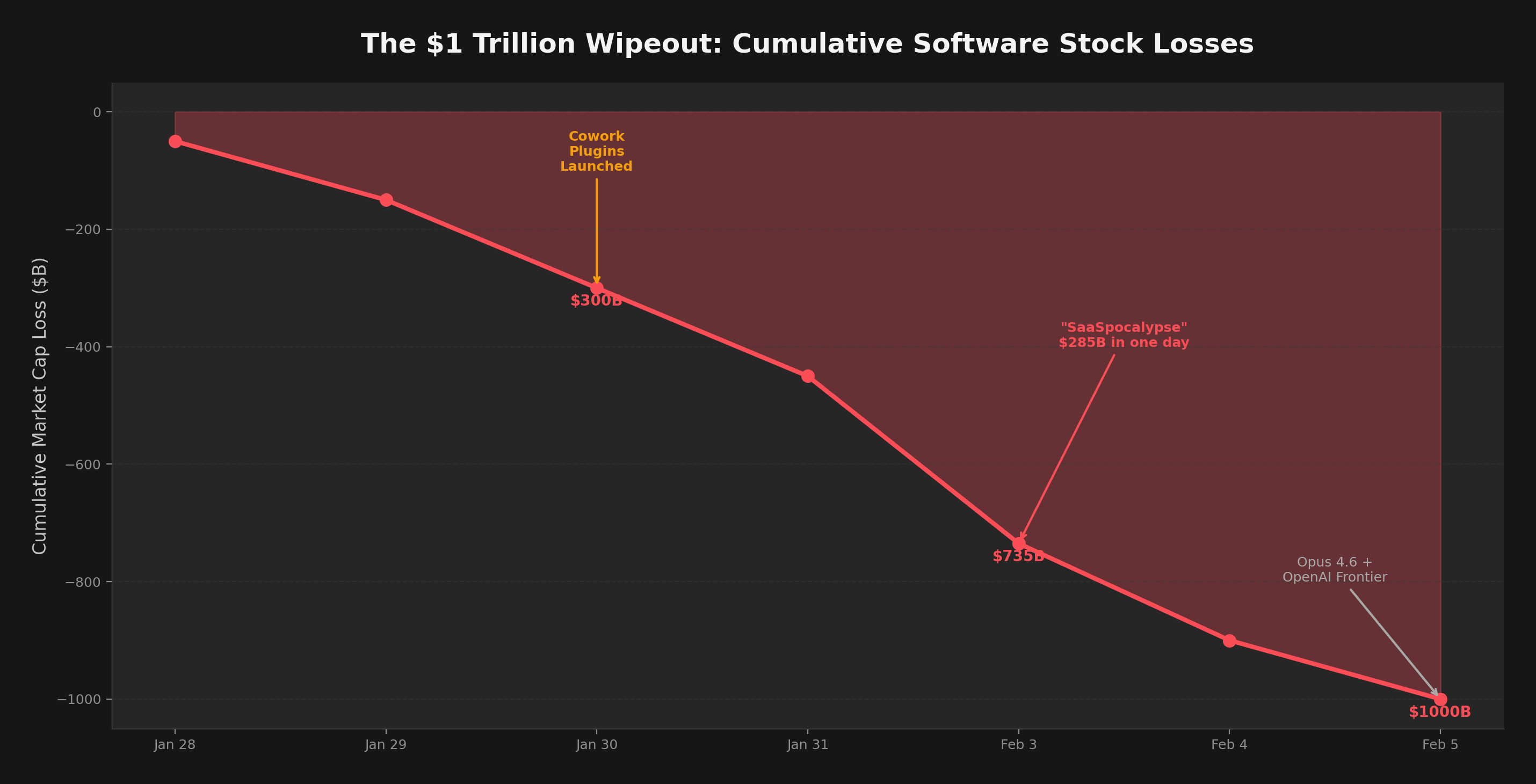

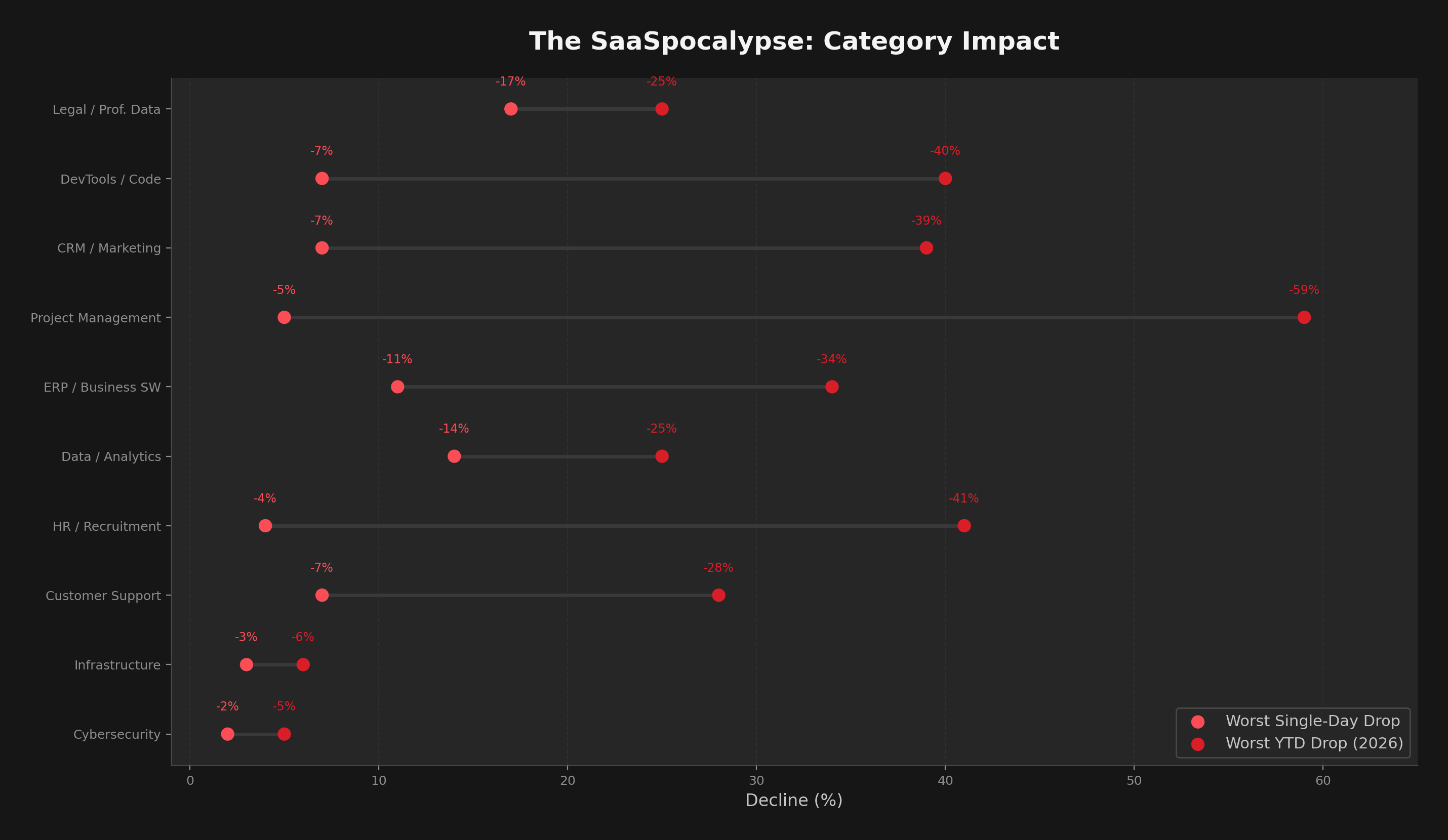

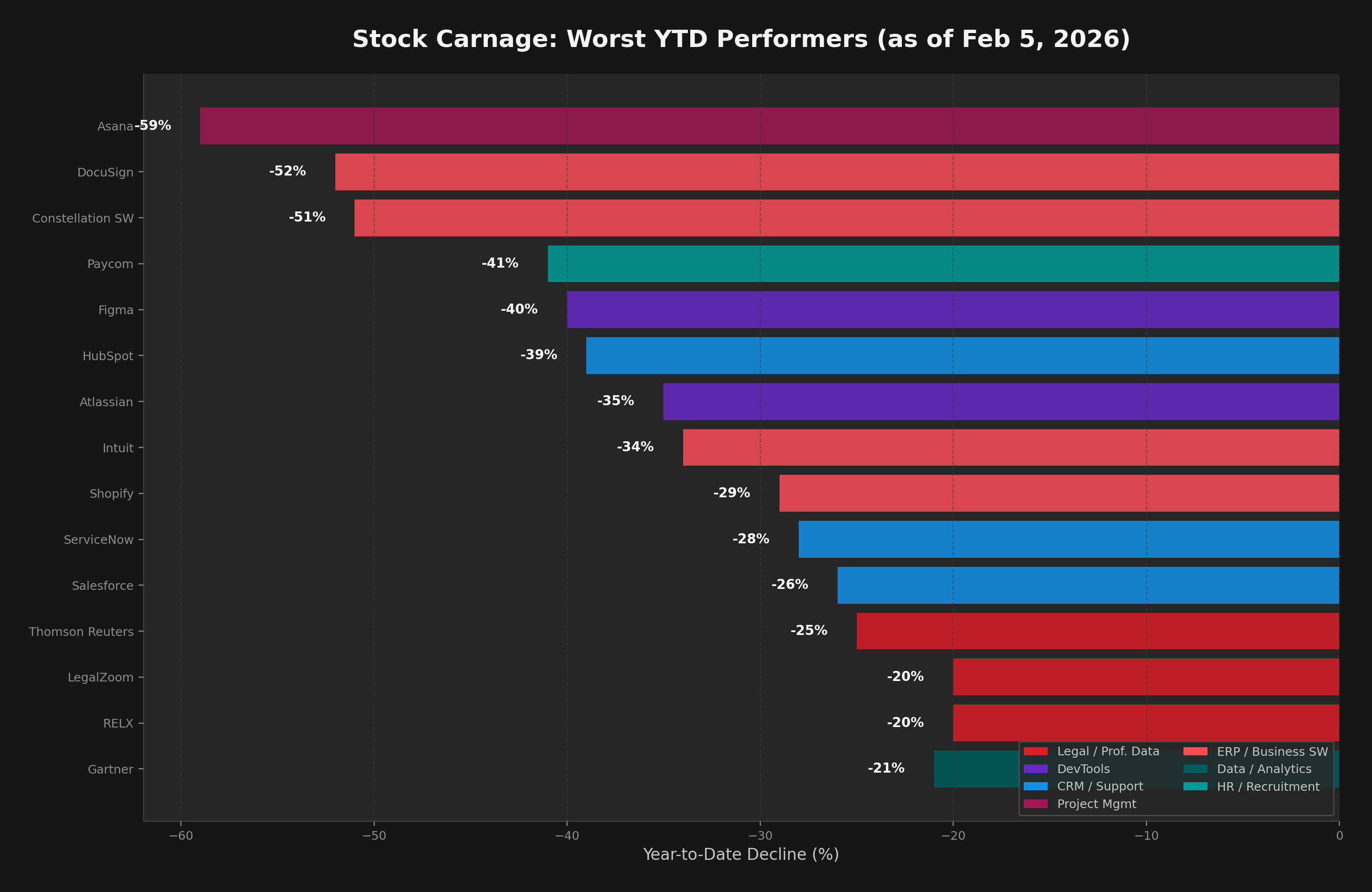

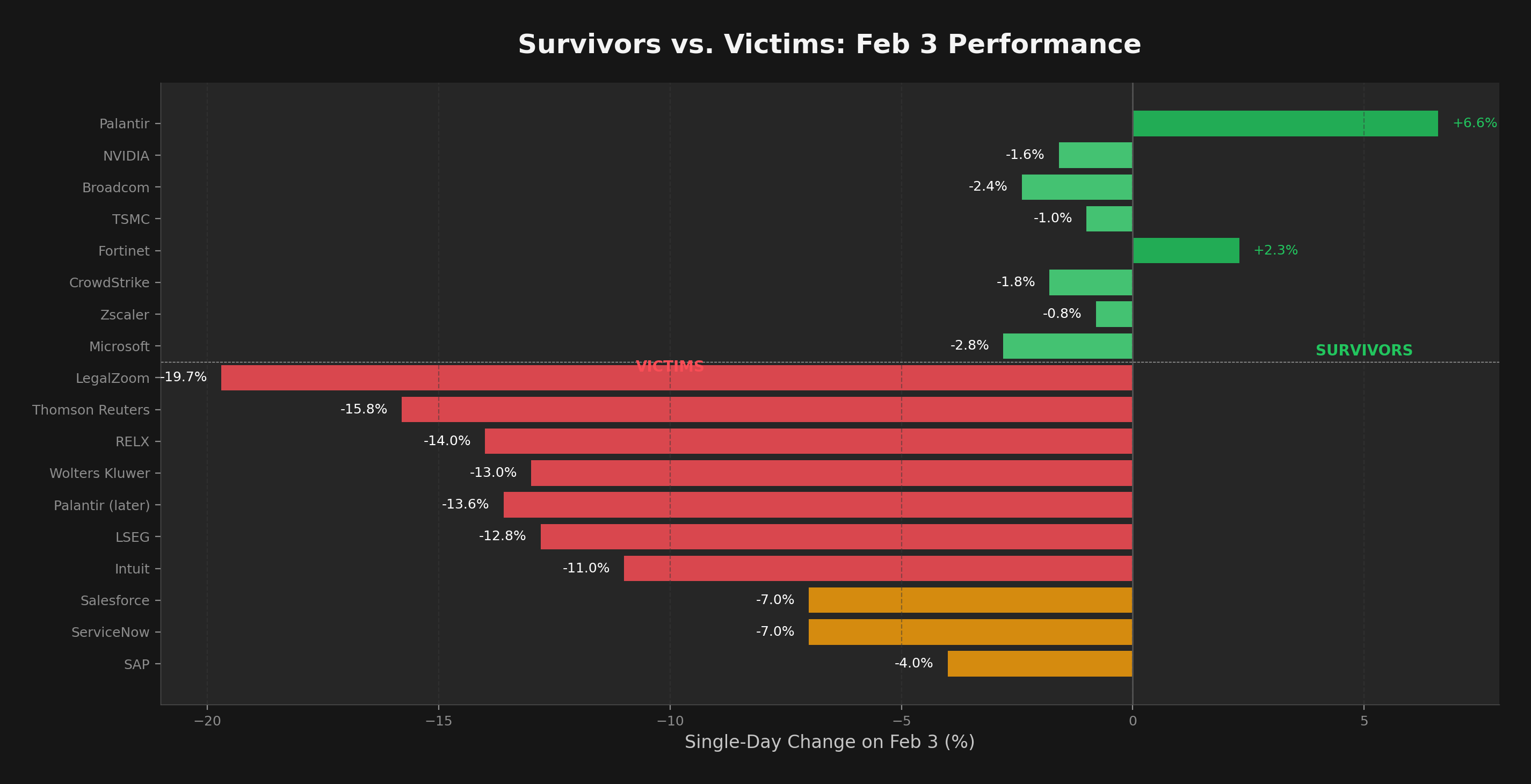

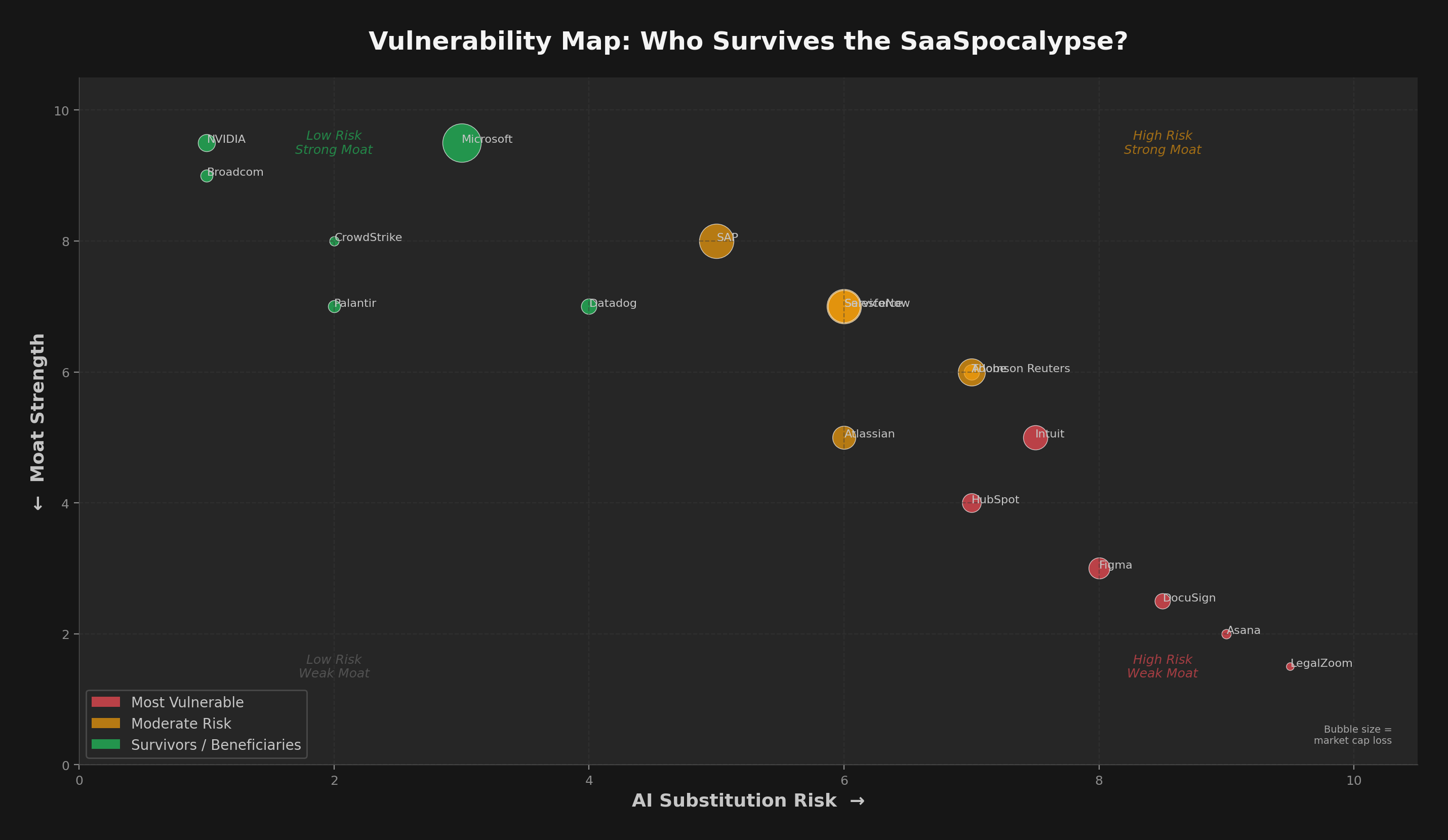

Part 3

The Infrastructure Layer: Cloud & ERP

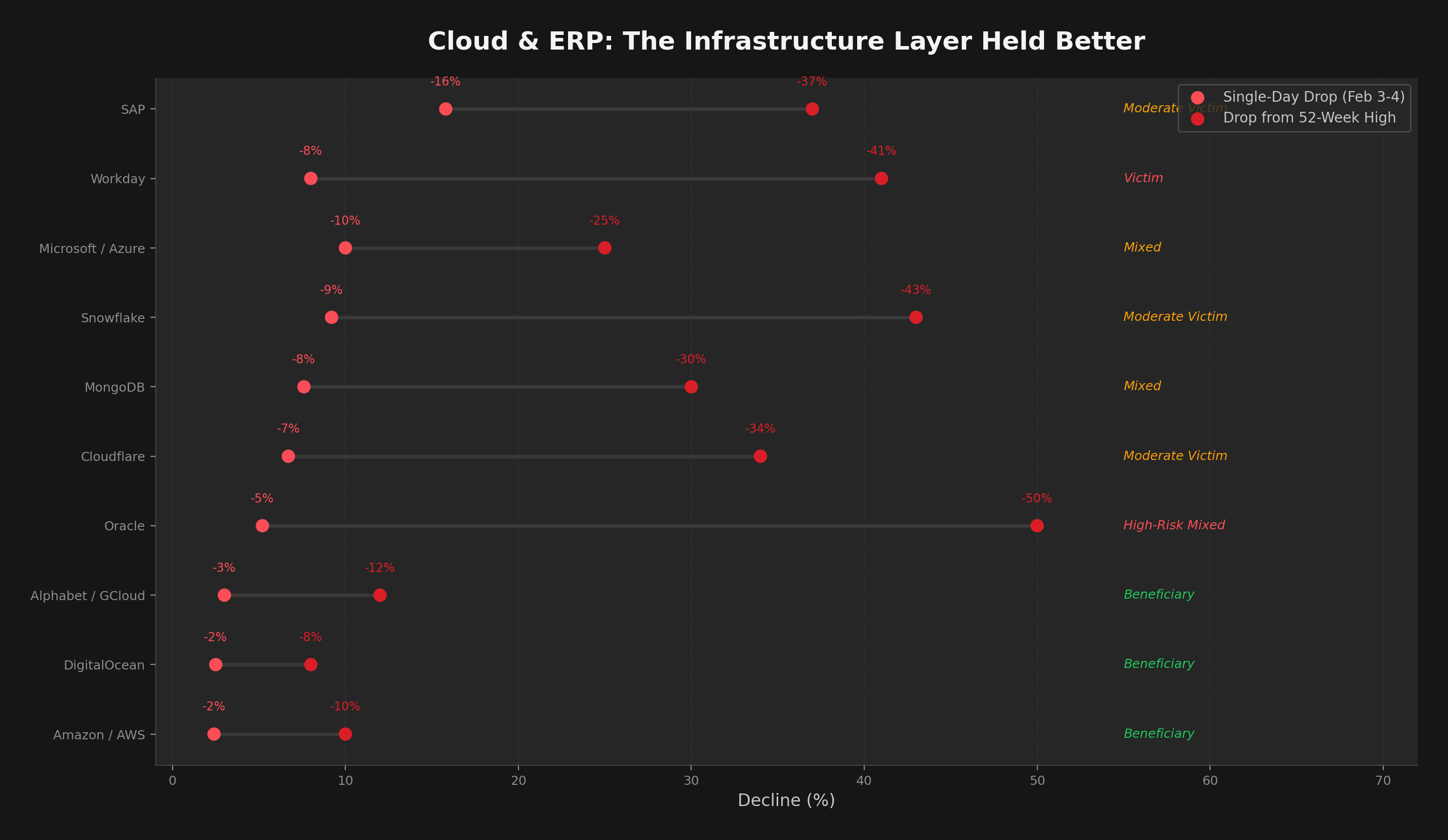

The most revealing pattern in the selloff is what happened to the infrastructure layer — the cloud platforms and ERP systems that sit beneath SaaS applications. The market drew a sharp line: pure infrastructure held, hybrid plays wobbled, and per-seat ERP got hammered.

Figure 3: Cloud and ERP companies plotted by single-day drop vs. decline from 52-week high. Pure infrastructure providers (AWS, Google Cloud, DigitalOcean) clustered in the low-impact zone. ERP and hybrid plays (SAP, Workday, Snowflake) saw far larger drawdowns.

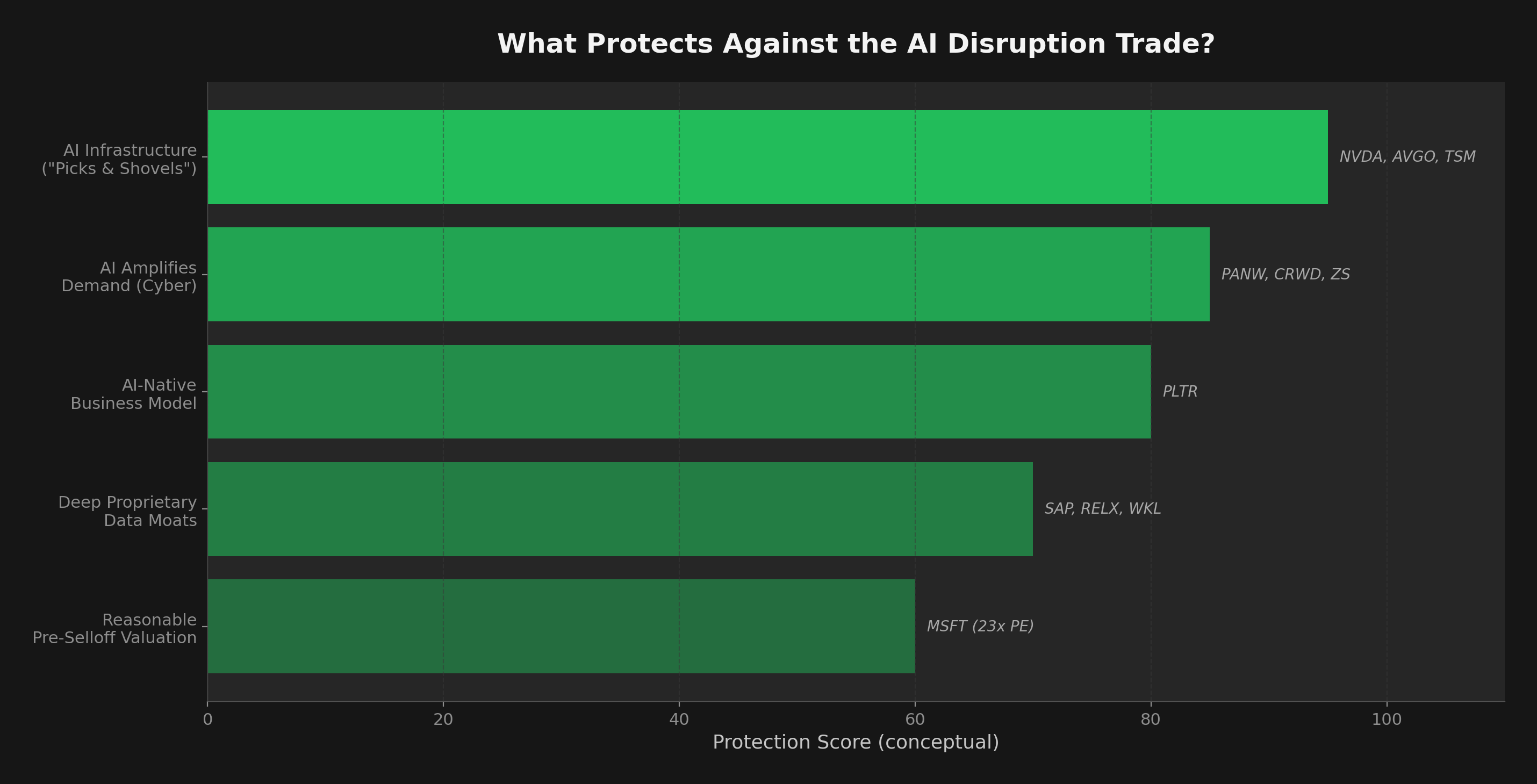

Hyperscalers: The Clear Winners

Amazon/AWS dropped just 2.4% on Feb 4 and remained positive YTD (~+4%). AWS is capacity-constrained, not demand-constrained — AI agents need compute regardless of which SaaS companies they displace. Alphabet/Google Cloud reported a 48% YoY surge in cloud revenue and a backlog that jumped 55% sequentially to $240 billion. CEO Sundar Pichai defended a staggering $175-185B capex plan for 2026, stating supply constraints — not demand — remain the binding issue.

DigitalOcean was the least affected of all companies researched (-2.5% single day). Bank of America upgraded it to Buy, noting its "drive into AI is leading to actual demand and significant operational leverage."

The Hybrid Middle Ground

Microsoft was uniquely caught between two narratives. As Azure, it's an infrastructure beneficiary (+39% cloud growth). As Office 365 and Dynamics, it faces SaaS seat disruption fears. The result: -10% post-earnings and -25% from peak. Stifel downgraded MSFT to Hold, though Seeking Alpha called the selloff "irrational SaaSpocalypse fears" given Microsoft's 27% stake in OpenAI (worth ~$135B).

Snowflake fell 9.2% on Feb 3 despite being a data platform, not a pure SaaS play. The "basket-style" selloff was indiscriminate. MongoDB dropped 7.6% — AI needs databases, but the market hasn't decided if MongoDB is infrastructure or a displaced middleman. Cloudflare fell 6.7%, though BTIG upgraded it to Buy the next day.

ERP: The Battleground

SAP faced a double whammy: disappointing cloud guidance and the SaaSpocalypse. It fell 15.8% on earnings (its biggest daily loss since 2020) with an additional 3.3% on Feb 3-4 — over $40 billion in market cap erased. Palantir's CTO publicly claimed AI could compress "complex SAP ERP migrations from years to 2 weeks," positioning AI as a direct replacement threat.

"AI agents will massively push the boundaries of the performance of SaaS solutions, but not replace them. There are about 20,000 legal jurisdictions worldwide and complying with applicable regulation is a major reason why people trust vendors like SAP."

— Christian Klein, CEO of SAP

Oracle presents the highest-risk profile: theoretically an AI infrastructure beneficiary, but weighed down by $250 billion in long-term leasing commitments tied to data centers and plans to raise $45-50B in debt for AI buildout. It's down over 50% from its September peak. Morgan Stanley warned Oracle's expansion leaves "little room for error."

Workday may be the most exposed ERP company (-41% from high). CEO Carl Eschenbach called the selloff "overblown" at Davos — but then announced $135 million in restructuring charges including layoffs, undermining his own defense.

The Infrastructure Lesson

The deeper the infrastructure layer, the safer the company. AWS and Google Cloud barely flinched because AI agents consume more compute, not less. Snowflake and MongoDB sit one layer up and got moderate hits. SAP and Workday are the application layer — exactly where AI agents threaten to replace human workflows and per-seat pricing. The market is pricing a clear stack hierarchy.